Programmatic DSPs

insights from management

Hello,

Earlier this week, I had a call with Michael Christenson, who has been CEO of Entravision ($EVC) since July 2023. I speak with management teams fairly often, but it’s rare that I come away as impressed as I did after this call.

Michael comes across as focused and tech-savvy, with a clear view of the long-term strategy and a willingness to make hard calls that are likely to be unpopular in the short term. He also runs corporate overhead extremely lean, understands how to build the repeatable systems required to scale the organization, and is pragmatic and disciplined when it comes to capital allocation.

I also like that he’s not promotional at all—his answers are honest, realistic, and backed by specific examples. He genuinely comes across as someone who keeps his head down and lets execution do the talking. That’s probably why you won’t find interviews with him online, and my guess is he wouldn’t have taken the call with me if I weren’t friends with one of the company’s largest shareholders.

I think his track record since joining Entravision speaks for itself, particularly in how he handled the strategic wind-down and execution in the AdTech segment, and in cutting corporate expenses by more than half.

He’s also put his money where his mouth is. After Meta shut down its ASP program—unfortunately taking roughly half of Entravision’s business with it—he bought shares aggressively in the open market and maintained the dividend. Earlier this year, he also cut his base salary and cash incentives in favor of more equity in the form of PUs and RSUs tied to stock performance, which makes me feel he’s very well aligned with shareholders.

The main reason I wanted to speak with him was to better understand the Smadex story since he joined Entravision: its value add, the competitive landscape, barriers to new entrants, the drivers of past growth, and the opportunity ahead.

As paid subscribers already know, Smadex matters so much because the risk-reward at $3.17 is very different from what it was when I first wrote it up at $1.93. That’s not because I think $EVC has become a pure Smadex bet, or that a slowdown in Smadex growth would kill the thesis. But Smadex has clearly become a much more important driver of upside from here than it was in the past, when it was growing more slowly, was less profitable, and made up a smaller share of the overall business.

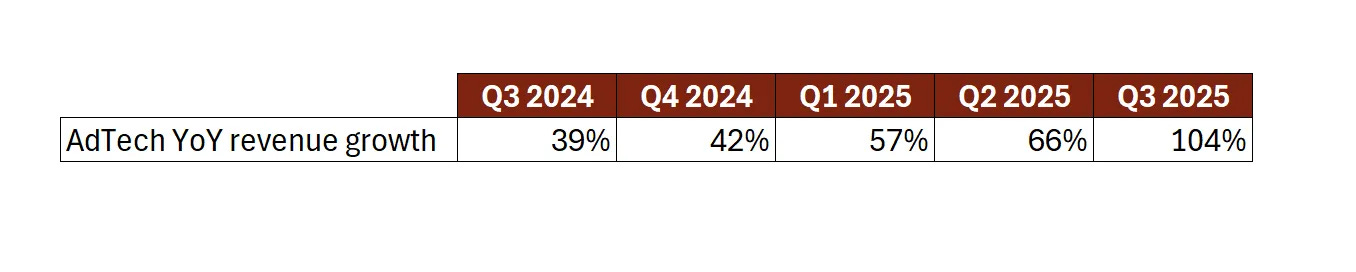

And even though Smadex and the broader AdTech segment now make up more than 63% of EVC’s revenue in the most recent quarter—and likely around 55% for the full FY 2025—with revenue growing 104% and EBIT up 378% before operating leverage has fully kicked in, I still think it is the variable of the thesis that the market underappreciates the most.

After all, AdTech’s EBIT for 2025 should come in at more than $25M, with a current run-rate closer to $40M, while $EVC’s entire enterprise value is still only around $440M. And what’s left isn’t worthless, but a highly FCF-generative broadcasting business focused on a politically important Spanish-language audience, along with the most valuable spectrum assets relative to EV among publicly traded traditional media companies I’ve looked at. We covered the current state of both on the call as well.

So without further ado, here are my notes from the call with Michael. I hope they do the conversation justice.