Groundbreaking Research

$MSV.AX, Mitchell Services UPDATE

It’s not ground breaking but it does feature a company that is breaking ground.

Just this morning, I spoke with Mitchell Services' CEO, Andrew Elf, and CFO, Greg Switala.

This is going to be a quick update covering ten of the most important highlights from the call, with some discussion about $MSV.AX downside protection and private market value at the end of the article.

If you haven't read my write-up yet, please stop reading and do so first:

Before I share the notes, I'd like to point out that both Andrew and Greg appear to be quite candid, answering all of my questions directly without deviating from the topic or trying to sugar-coating the picture. This is a rare quality to find in managers nowadays.

Let’s get going.

Comments regarding industry's consolidation over the last 5-10 years and the competitive situation among drillers

Perenti leads the West Coast, while Mitchell leads the East. Both companies have consolidated their respective markets with numerous acquisitions over the previous decade, and, competition wise, the industry is in a much better space now than has been the case in the past.

Perenti has a lesser portion of their business on the East Coast as well; however, AJ Lucas is their primary competitor there.

At the moment, it's very very hard to start a drilling company and get Tier1s “onboard”

Thoughts on the cycle in the last few years

Things have improved to a certain degree from the pre-pandemic period. They have come back since then and now remain "flat" for some time.

On why have they historically used more equity than debt for financing? Thoughts on capital allocation going forward, now that virtually all debt has been paid off

Acknowledged the fact that ideally you don't want to use equity. Think it would be a step too far if they had done everything with debt in the past as the balance sheet would worsen. They have absolutely no intention of raising equity going forward.

Aside from the targeted 75% payout ratio, they are patient with how they employ generated cash flows. They don't believe there's a need to strengthen the balance sheet any further and are waiting to see how the expected short-term trial for decarbonization solutions with their first client unfolds over the next few months. If the results aren't as encouraging and they don't see adequate growth capex returns in that space, they will buyback more stock.

On whether they believe utilization percentages could ever sink again to 30-50% levels that they experienced from 2014-17, or if that is impossible now due to increased client diversification

It can always drop off, but with the current balance sheet, they don't view it as a problem. Utilization wise, they'd rather have fewer rigs running well than more rigs running poorly.

On gold drilling activity over the last few months, following the latest gold spike. How is the junior mining space for gold looking like right now?

It's definitely still muted. Producers are busy but are not asking for extra rigs.

The future of gold activity is the most frequently discussed topic in the industry.

Equity markets are still tough to access for junior miners.

On differentiation of their rig fleet and whether gold rigs could be utilized for coal drilling and vice versa

The 10 rigs used for underground coal drilling are the most technical in nature and can only be utilized for coal. Underground mineral rigs can be used for either.

For surface drilling, it depends; surface coal is a bit more technical, while other surface rigs usually face more competition and can be used for multiple commodities.

The geotechnical work they do is highly specialized

On what they see as the largest risk to the business

Safety. Mines collapsing, mines blowing up. Things they can't control.

On which client or competitor could cause you most trouble if they chose to

Any of their large clients could harm them if they wanted to. Clients have a far stronger bargaining position and could even propagate damaging rumors throughout the industry.

They aren't really concerned about competition.

On if they believe that diminishing deposit grades / reserves will result in increased demand for drilling in the longer term

There's been a level of inactivity in the space in recent years. They think large producers will need to either combine via M&A or do more drilling if the consolidation doesn't work.

And I'm leaving the finest one for last.

I noticed a note in the annual report stating that the book value of rigs on the balance sheet is understated in comparison to their market value. What would you say is the current average market value per rig?

The replacement value per rig is 2M, while the market value of their entire rig fleet is roughly 120M.

Talking my book (value)

Let’s do more math on that front. The current book value of MSV is 66M, and the current net PP&E amount stated on the balance sheet is 63M. If we increase the PP&E to 120M, the actual fair market value of Mitchell's rig fleet, we get an adjusted book value of 123M.

That is, at the current market cap of 85M (including ESOP), MSV is selling for 0.7x P/B.

Also, if another company decides to compete in the drilling industry and begins building a similar rig fleet from scratch. With the current fleet of 93 rigs (excluding five older rigs), it would cost 186M to build a fleet the size of Mitchell's. Pushing P/replacement value of MSV to an even lower multiple.

If you perform the same calculation, adjusting the net PP&E to replacement cost and then the book value, you would see that MSV is trading for about 45% of its replacement cost.

Private market value

Aside from the "normalized owners earnings" work outlined in the last write-up, I spent some time this week researching acquisitions in the drilling sector during the last six years. This could provide me with another rough estimate of what MSV may be worth today if sold to another buyer.

At the current multiple of 2.2x EV/EBITDA, MSV is trading at a 56% discount to the average acquisition EV/EBITDA multiple and a 51% discount to the median one. This means that a typical potential acquirer would be ready to pay around double the current market cap to acquire MSV.

If you wish to make it a bit more conservative, you can slap a 20-30% control premium (discount) on acquired companies and proceed from there.

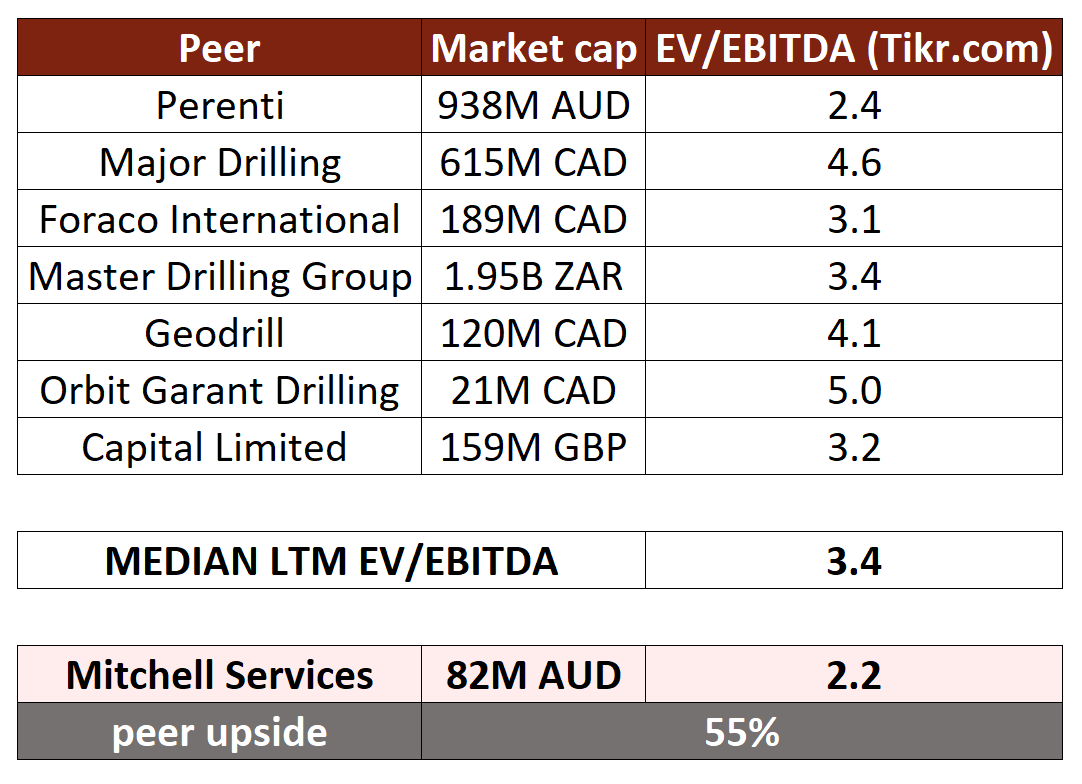

Premium or no premium, this is another indicator confirming how cheap Mitchell is today. To take it a things a step further, I've chosen to do something I usually avoid. A peer analysis.

The rationale behind this decision is do a sanity check and to determine whether MSV is an outlier even when compared to their peers, the ones who operate in this industry most investors deem disgusting.

Yes, MSV is cheap even when compared to the already cheap drilling industry.

It's crucial to note that, while all these companies have capital structures and business models quite comparable to Mitchell's, peer analysis is not without its problems.

For example, Perenti is more than just a driller, as DDH1 was when Perenti acquired it, but a diversified mining contractor.

Also, while all of these companies are exposed to gold, none are as strongly exposed to met coal drilling as MSV. Aside from gold, there is higher exposure to copper, silver, lead, or battery metals, thus, it is not an apples-to-apples comparison

My initial diligence work ends here, and my main conclusion remains the same. MSV is a business that has undergone substantial change over the years and is now undervalued on all metrics.

EV/normalized FCF, EV/EBITDA, P/adj. Book, P/replacement value, P/PMV, and when compared to relevant listed peers. (and if you read the prior write-up, you would understand why I chose EV/EBITDA.)

It's an even easier bet to make now that I trust the management's operational and capital allocation skills.

Is there something I missed? Probably, I'm not following the industry that closely.

Will that detail(s) affect the risk-reward equation? I highly doubt it. At this market cap, the bet is rigged (pun intended) in my favor.

That’s it for this short update. Thank you for reading!

disc: still a ~3% position

This is NOT investment advice. All content on this website is for entertainment, informational, and educational purposes only and should not be considered to be advice of any nature. Due your own due diligence.

Loved this article. On the acquisition multiples, it's worth noting the Swick, DDH and Perenti multiples were all script (Perenti had a minor cash proportion with script the majority), which meant the multiples were lower. It is hard to see the Mitchell family giving up control (though I guess same could have been said for Kent Swick) so I think a premium is warranted for valuation purposes. For me a rough rule of thumb for ASX listed drillers is to buy when div yield is around 10% (worked really well in the past for me), which is the case for MSV now. Ultimately Australian investors have a strong bias for dividends and at some stage if/when MSV start paying franked dividends, then expect share price could react well.

Great article - did you discuss falling oil prices and the impact on the business?